Published on 03 November 2022

First published in 1993, the KPMG Survey of Sustainability Reporting is produced every two years. This year’s edition provides an analysis of the sustainability and Environment, Social, and Governance (ESG) reports from 5,800 companies across 58 countries and jurisdictions. It is one of the most comprehensive and authoritative pieces of research on sustainability reporting worldwide.

Key findings of the latest global survey

- Sustainability reporting has grown steadily, with 79 percent of leading companies providing sustainability reports

- Improved reporting of carbon reduction targets, but action remains too slow in key areas and fewer than half of companies currently recognize biodiversity loss as a risk

- Fewer than half of the world’s largest companies are reporting on ‘social’ and ‘governance’ components of ESG

- KPMG’s recommendations include shifting from a narrative-driven approach and making better use of data to drive change and provide evidence of action

Key findings for Belgium

- The application of and adherence to reporting standards can be further improved for Belgian companies, which lag behind their global peers in this respect

- Only 1/3 of Belgian N100 companies that report on sustainability are obtaining third-party assurance on their reporting

- Belgian companies need to further integrate ESG-related risks and opportunities into their risk management

- Although almost 2/3 of Belgian N100 companies report on carbon reduction targets, only 1/3 of Belgian companies have adopted or intend to adopt science-based targets

- Belgian companies reporting non-financial information continue to extensively link the UN Sustainable Development Goals (SDGs) to their business but need to improve communication on both the positive and negative impacts of their activities on the SDGs

- Belgian companies are further integrating sustainability into their governance structure and ESG performance is increasingly linked to Board and executive compensation

- KPMG strongly recommends that Belgian companies already invest in identifying critical gaps in current reporting and ensuring reliable and accurate ESG data can be reported and assured, to prepare for compliance with the Corporate Sustainability Reporting Directive (CSRD)

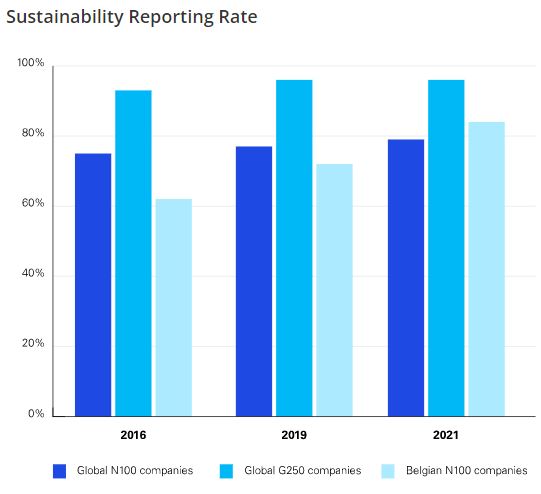

Sustainability Reporting

As in previous surveys, in 2022 we analyzed the sustainability reporting of financial year 2021 for the 100 largest Belgian companies (Belgian N100). The reporting rate of Belgian N100 companies rose from 62% in 2016 and 72% in 2019 to 84% in 2021 compared to 79% for the N100 global average (up from 75% in 2016 and 77% in 2019).

However, much improvement is still needed, especially compared to the reporting rates of the largest 250 global companies (G250), of which 96% (stable compared to 2019) are reporting on their Sustainability activities and considering that all large undertakings will need to report extensively on their sustainability performance following the upcoming Corporate Sustainability Reporting Directive (CSRD) adoption.

Reporting standards

The adoption of the Global Reporting Initiative (GRI) Standards is still showing a consistent increase for the G250 and Global N100 companies. However, in Belgium, we observe a decline of 5% (from 37% in 2019 to 32% in 2021) in N100 companies that state they are reporting “in accordance with” the GRI Standards. Additionally, 19% of the Belgian N100 companies are referring to the Sustainability Accounting Standards Board (SASB) Standards. Taking these percentages into consideration, reporting standards application in Belgium can still be improved significantly. For both the global N100 and the G250, GRI and SASB reporting rates are still considerably higher than those of the top Belgian companies.

As for the application of integrated reporting, global and local rates remain equally low: only 15% of Belgian companies state that they are following the International Integrated Reporting Framework or guidance from the International Integrated Reporting Council (IIRC), which is in line with the global average of 13% of all N100 companies.

Third-party assurance

Barely one-third of Belgian N100 companies that report on sustainability are obtaining third-party assurance on their reporting, which is an increase of a mere 4% compared to 2019 reporting. A vast majority obtains assurance on just part of the report, such as on specific indicators. The Belgian assurance rate remains significantly lower than the average global N100 companies (47%) and the G250 (63%) reporting on sustainability. To meet the ever-growing request from stakeholders and investors for the availability of reliable, robust, and comparable sustainability information, this assurance rate needs to increase considerably. Additionally, the companies in scope of this survey will be subject to the upcoming CSRD which imposes mandatory assurance on the sustainability information reported. There are still large hurdles for many of these companies to overcome if they are to be prepared in time for the CSRD.

Integration of sustainability information into the management report

64% of Belgian N100 companies publish a stand-alone sustainability report, while 68% have included ESG/Sustainability information in their annual report (compared to 60% of N100 baseline globally). One of the expected requirements of the CSRD will be the inclusion of the sustainability-related information in the management report of the company. Only 51% of the N100 companies in Belgium identify material topics in their reporting. Compared to the Global N100 companies (56%) and G250 companies (74%) that report on sustainability, Belgian companies continue to lag behind.

The UN Sustainable Development Goals (SDGs) in non-financial reporting

Our survey further shows that Belgian companies that already report on non-financial information continue to extensively report on the SDGs most relevant to their business (81% compared to prior 76%). Belgium is currently still outpacing the global N100 average (71%) and G250 (74%) in this respect.

The SDGs most frequently identified by Belgian companies were:

- SDG 3 Good Health and Well-being,

- SDG 8 Decent Work and Economic Growth poverty, and

- SDG 13 Climate Action.

However, only approximately 16% of the N100 Belgian companies reporting on sustainability communicate both their positive and negative impact on the SDGs, which is consistent with the percentages revealed in our 2019 survey. Additionally, only 32% of the Belgian companies reporting on sustainability disclose performance goals related to the SDGs, up from 29% in 2019 reporting. This is consistent with the global N100 and just below the G250 companies (37%). With the implementation of the CSRD, companies will not only need to disclose meaningful targets but will also need to report on their positive and negative material actual or potential impacts.

Integrating ESG into risk management

Companies will further need to integrate ESG-related risks and opportunities into their risk management. Currently, barely half (52%) of the Belgian N100 companies acknowledge climate change (e.g. transition risks, physical risks), with even fewer (43%) citing social elements (e.g. risks relating to health & safety, diversity & inclusion) and (41%) governance elements (e.g. risks relating to bribery and corruption, business conduct) as risks to their business in their annual report.

There is a growing acknowledgement of the financial risks associated with climate change. As indicated above, 52% of the largest Belgian companies report that they have acknowledged climate change as a business risk, up from 30% in 2019 reporting. In describing the potential impacts of climate-related risks, the majority make use of a narrative (45%), although a few companies are also applying financial quantification (2%) or scenario-analysis (5%). 23% of the Belgian N100 are stating that they report in line with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD). Although we observe a significant increase compared to 2019 (9%), Belgium is clearly lagging behind compared to the global N100 (34%) and especially G250 (64%). However, climate change is considered by CEOs as a key risk to growth in the KPMG 2022 CEO Outlook. Additionally, the key worldwide sustainability reporting proposals – CSRD, ISSB, and SEC – have largely incorporated the recommendations of the TCFD.

In 2021, 25% of Belgian N100 companies recognized the loss of biodiversity/nature as a potential risk to their businesses. In this respect, Belgian companies will need to further catch up with the global average (31%) and the G250 (44%). We note that companies in scope of the CSRD will also need to report disclosures in relation to biodiversity and ecosystems in the near future, with biodiversity loss considered a key environmental risk under the Directive. The Taskforce of Nature-related Financial Disclosures (TNFD) is currently also developing a risk management and disclosure framework to place greater emphasis on this aspect of environmental risk and impact.

Carbon reduction targets

A growing number of companies are disclosing carbon reduction targets in Belgium. 64% of the N100 companies report on carbon reduction targets (+21% vs. 2019) compared to 59% of global N100 and 76% of G250 companies. 49% of companies also link these carbon reduction targets to global, regional, or national carbon targets (+19% vs. 2019). However, only one-third of the largest 100 companies in Belgium have also adopted or intend to adopt science-based targets for carbon reduction as defined by the Science Based Targets initiative (SBTi). This is in line with the observed percentages of the global N100 (25%) and the G250 (35%).

ESG Governance

It’s still only the beginning of the involvement of top management in addressing ESG risks – and ESG governance more generally - both in Belgium and worldwide. We observe that 30% of the N100 companies in Belgium acknowledge in their annual report that a dedicated member of the Board and/or leadership team is responsible for sustainability matters, compared to 34% of global N100 companies and 45% of G250 companies.

It is clear that companies are increasingly integrating performance on sustainability matters into the variable compensation of board or leadership members. 30% of the Belgium N100 companies acknowledge in their annual report that a sustainability matter has been included in the compensation, either at the Board or leadership team level, compared to 24% of the global N100 companies and 40% of the G250 companies.

A call to action

New ESG requirements are driving a different perspective and set of conversations in Boardrooms, pushing business leaders to stretch their thinking and ensure that from the top down they are making strategic decisions that take climate and broader ESG considerations more into account.

Considering the increased focus of investors and stakeholders on sustainability matters, as well as the upcoming legislative reporting proposals, it is key that companies take the next steps in their sustainability journeys and prepare thoroughly for the new trends and requirements. The pressure on businesses to report on non-financial metrics is only expected to grow as regulations evolve. By acting now, companies can make informed choices to drive the change that is much needed to be a good corporate citizen in today’s world.

It will be crucial for companies to already take the necessary steps by integrating sustainability into their business operations, governance structure, and risk management. Identifying critical gaps in their current reporting and making sure to fill these gaps in time, as well as ensuring reliable and accurate reporting of sustainability information and data (by setting up robust reporting processes, systems, and structures), will prepare companies for the future.