Published on 17 March 2022

Consumer and Retail leaders remain optimistic on growth prospects amid challenges

As evolving consumer expectations, the accelerated pace of change and the impact of COVID-19 continue to challenge businesses, the KPMG 2021 CEO Outlook Survey reveals that global business leaders remain optimistic about their growth prospects and their pursuit of digital transformation.

But what’s dominating CEO agendas in the consumer and retail (C&R) industry as their organizations address today’s challenges while looking ahead to success in a bold new era of competition and opportunity? Below, we summarize the responses from C&R CEOs who participated in the survey.

C&R CEOs are upbeat about their future growth prospects. A total of 86 percent say they are ‘confident’ or ‘very confident’ about their organizations’ growth over the next three years. And how do they expect to achieve their growth objectives over the next three years? Among all growth strategies, 36 percent of C&R CEOs are focused on strategic alliances with third parties. Organic growth (via innovation, R&D, capital investments, new products, and recruitment) was close behind, cited as a key strategy by 34 percent of C&R CEOs.

What specific activities will C&R CEOs turn to in their pursuit of growth over the next three years? Their playbook includes the following priorities:

- A total of 74 percent plan to increase investment in new disruption-detection and innovation processes.

- Joining industry consortia focused on development of innovative technologies is on the agenda for 64 percent.

- More than half (58 percent) are looking to make their products and services available via an online-platform provider, including social media. And about one third (32 percent) will partner with third-party data providers.

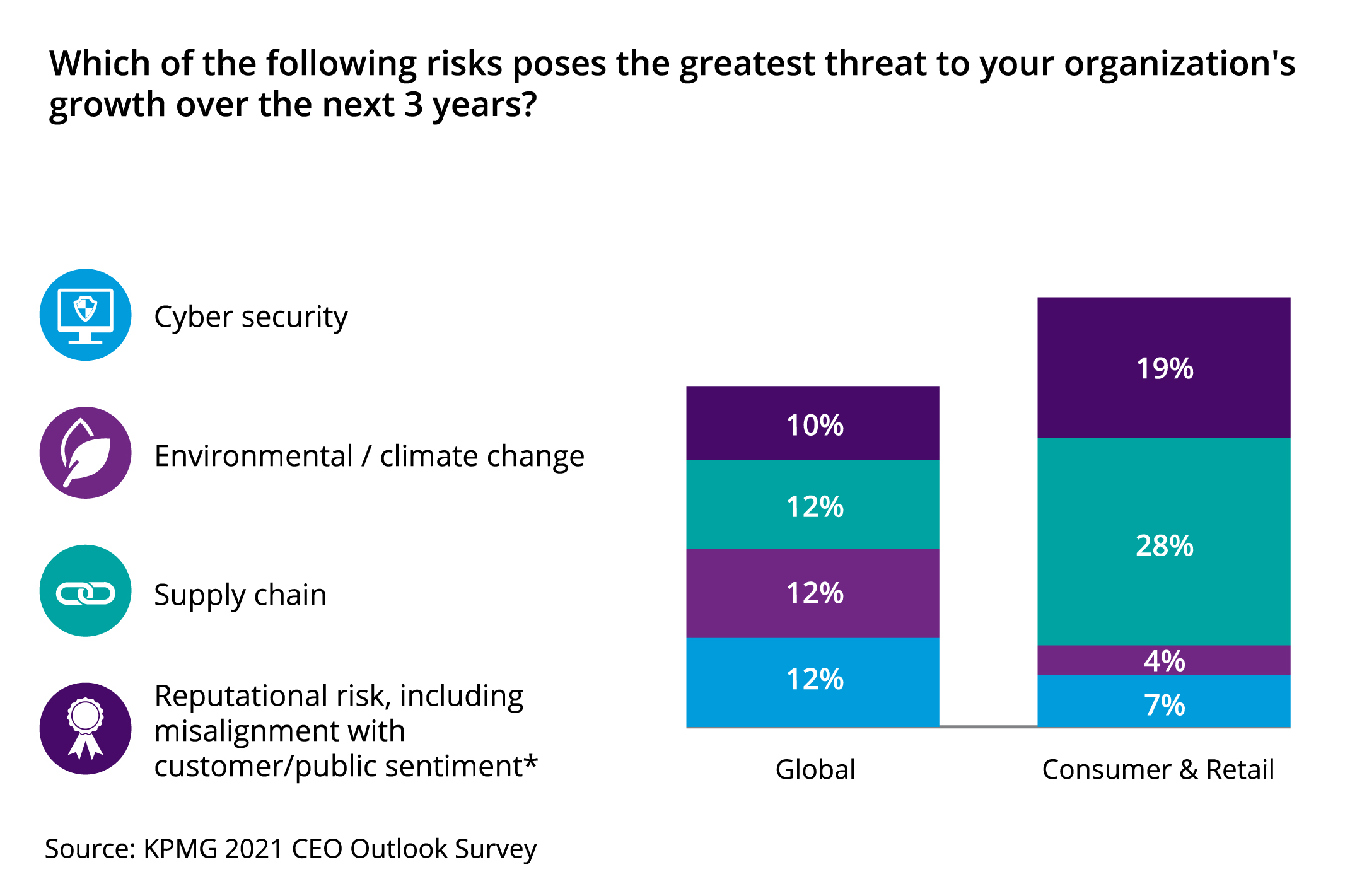

In the pursuit of growth, we also need to address the risk to growth. Below we discuss the challenges on supply chains but also to note about one in five C&R CEOs also view reputational risk as a key growth threat, this was nearly double of leaders in other sectors. In today’s customer-centric driven marketplace C&R leaders are focused on the health of the planet, health of consumers and the opportunities and disruptions from digitization.

The transformation race continues

The focus on digital transformation and customer centricity remains intense for C&R businesses in today’s hypercompetitive, fast-moving markets. And while many businesses are working hard to drive change, the survey reveals that C&R CEOs recognize the need to move faster to enhance capabilities and meet ever-evolving consumer expectations.

- Making agility a priority: Eighty-one percent of C&R CEOs believe they need to be quicker to shift investment to digital opportunities and divest businesses that face digital obsolescence. Seventy-seven percent also agreed with the statement: “We have an aggressive digital-investment strategy, intended to secure first-mover or fast-follower status.”

- Viewing disruption as an opportunity: C&R leaders are telling us that there’s no time to lose. They have a heightened sense of urgency as retailing continues to undergo a historic transformation and are confident in their ability to make progress. A significant majority (79 percent) also view technological disruption as more of an opportunity than a threat. And 74 percent agreed that, rather than waiting to be disrupted by competitors, their organization is actively disrupting their sector.

- Shifting investment priorities: As a result of accelerated pace of change, the pressure is on to rapidly respond, innovate and evolve if they hope to compete. To help meet their growth and transformation objectives, investment priorities for C&R businesses are increasingly balanced between skills and technology investments: 53 percent are more focused on investments in new technology, and 47 percent are looking at greater investments in new digital skills and capabilities.

- Forging new partnerships: Most don’t plan to go it alone. To drive transformation, a slightly higher percentage of C&R CEOs are looking to forge innovative new business partnerships that will be critical to sustaining the pace of digital transformation compared to all global CEOs. Innovative partnerships will likely prove beneficial over the next three years as organizations continue to stabilize in the wake of the pandemic. The question for many is whether to build, buy or partner in order to rapidly implement the digital capabilities needed to compete in a bold new era of customer-centric service and personalization. Most (64 percent) view new partnerships as critical to sustaining the pace of digital transformation post-pandemic. Smart organizations realize a new ecosystem of partners can help them succeed on their journey.

- Offering greater flexibility: As they continue to respond strategically to the pandemic, 53 percent will also consider shared office spaces to give employees greater workplace flexibility. At the same time, half of respondents will be looking to hire talent that works predominantly remotely, — which aligns with the overall global findings.

Supply chains pose significant challenges

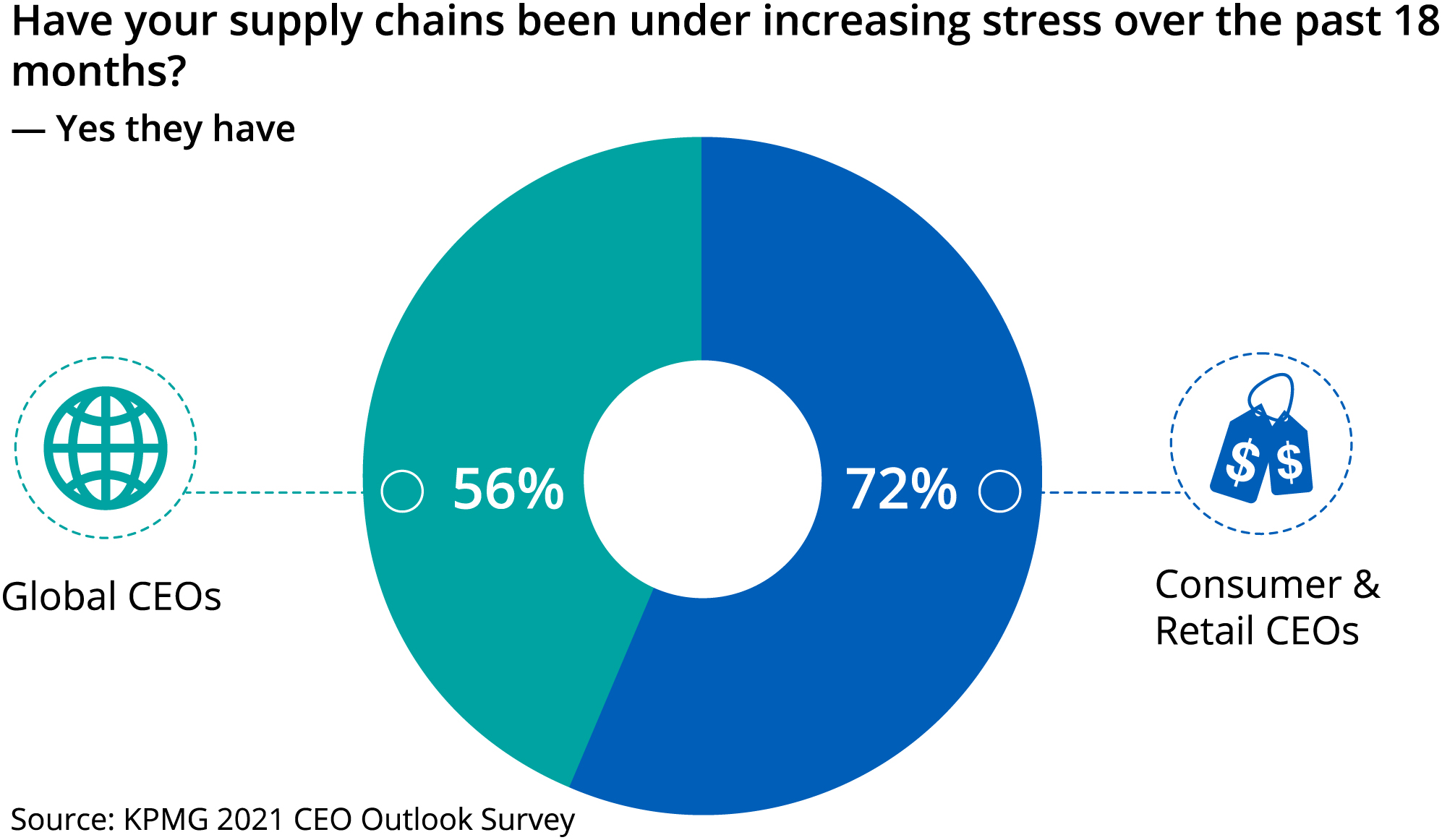

While business leaders are optimistic, they face significant supply-chain challenges that may demand strategic solutions. Nearly three quarters of C&R CEOs said their supply chains have been under increasing stress over the past 18 months — significantly higher than leaders in other industries.

- Threats to growth: Supply-chain risks are seen as posing the greatest threat to growth over the next three years among 28 percent of C&R leaders. We also highlighted reputational risk as a key growth threat. That’s perhaps not surprising in today’s customer-centric, social media-driven marketplace, as C&R businesses manage their public perception. And despite the continued emergence of game-changing digital capabilities, only 7 percent cite cyber security as a significant growth threat, which is seems to be very low also compared to other sectors.

- Increased supply-chain monitoring: With supply-chain challenges top of mind for C&R leaders, how will their businesses respond? To mitigate supply-chain issues over the next three years, 33 percent said their top strategy will be to monitor supply chains more deeply — at the third and fourth levels — to better anticipate potential problems.

- Resilience and skills among operational priorities: Supply-chain resilience will also be a high operational priority in meeting growth objectives over the next three years. About one fifth cite reconfiguring supply chains for greater resilience among their operational priorities — significantly higher than all other sectors. More than one in five also say operational priorities to support growth include plans to enhance employee value propositions in order to attract and retain talent and critical new digital skills. That reflects the C&R sector’s need to capitalize on new digital and data analytics capabilities with modern skills. Just 8 percent of leaders view cyber-security resilience as an operational priority, compared to 16 percent overall.

The demand for ESG transparency

C&R sector leaders also face demand from stakeholders, such as customers, investors and regulators, to increase reporting and transparency on environmental, social and governance (ESG) issues, with a total of 54 percent citing ‘significant’ or ‘very significant’ demand in this area.

- Reporting needs on the rise: More than one quarter also say they struggle to meet the ESG reporting needs of different investors and other stakeholders. And a similar number say their ESG performance reporting lacks the rigor of their current financial reporting. Integrating ESG reporting into current measurement and reporting processes is cited as an operational priority for only 11 percent of C&R CEOs.

- Impact on financial performance: Regarding the impact of ESG programs on financial performance, 31 percent say their ESG initiatives ‘improve’ or ‘significantly improve’ performance. But 41 percent believe the impact is neutral or negligible, while 28 percent say their ESG program ‘reduces’ or ‘significantly reduces’ financial performance.

- Telling their ESG story: At the same time, the vast majority (83 percent) say they want to “lock in” the sustainability and climate change gains made as a result of the pandemic. But effectively communicating ESG performance to stakeholders is posing challenges for some, with 37 percent of C&R leaders saying they struggle to articulate a compelling ESG story.

Key takeaways

While C&R CEOs approach the future with an ambitious air of optimism about their growth prospects, they maintain an aggressive stance on transformation amid profound marketplace changes which require an accelerated pace of change and focus on customer centricity. We believe the best C&R CEOs will be:

- Investing more quickly and effectively in powerful new digital capabilities that enable them to compete in customer-centric personalization whilst also driving cost efficiencies.

- Setting up their leadership and processes to be able to quickly solve supply-chain challenges to meet customer demand despite disruptions.

- Pursuing smart strategies that make products and services more widely available via online platforms, with seamless customer experience transferred between offline and online.

- Enhancing employee value propositions, including offering new ways of working and strong purposeful and purpose-driven roles, that attract, retain, and develop global talent.

- Establishing strategic alliances and partnerships, including working with industry consortia being high on the agenda to accelerate transformation into smart, responsive, data-driven businesses.

- And pursuing environmental and societal goals in both investment decision making and everyday decision making, to deliver truly sustainable growth for the health of both planet and consumer and driving the way on a greener future.