Publié le 30 août 2022

In a fast-evolving market, where businesses face new challenges and disruptive changes, their focus should be on increasing agility, managing risks, and building resilience for whatever the future holds. In other words: to be trusted by their stakeholders, organizations need to embed a balanced approach to risk and regulation into their transformation.

In turn, that trust enables responsible growth, bold innovation, and high performance. Kathy Lim, Tax Director, Tim Vermeiren, Audit Partner, and Benny Bogaerts, Head of Digital Risk Management, offer their insights on becoming a trusted organization.

Trust has become an imperative

“Trust is one of the most powerful business enablers”, stresses Kathy. “The confidence of stakeholders in your organization will drive growth, performance, efficiency and innovation. Trust is built on consistent, predictable action in the moments that matter. It touches every aspect of your business: from brand reputation to regulation and reporting – from ESG to digital transformation and customer experience.”

“We’re living in a fast-evolving business world, on the heels of a global pandemic and digital transformation. All too often, risk and regulation management are afterthoughts”, says Benny. “If you consider them as hurdles that slow down growth, think again. Addressing risk and regulation in a disciplined way, through the eyes of stakeholders, can drive growth – for example, to confidently develop new technologies, markets, and customer experiences. People want to do business with and work for organizations they trust. For organizations, trust is the ticket to play.”

“As the enterprise evolves, risk monitoring should be an ongoing process. It should go beyond reactive defense and passive compliance, and towards actively anticipating risks and opportunities”, continues Tim. “That’s how you inspire stakeholder trust and help create a successful future that is also sustainable.”

To whom?

Enterprises build trust with various types of stakeholders. “There are external stakeholders, such as customers and shareholders”, says Kathy. “They expect transparency and integrity in terms of economic contribution towards societies that corporations operate in. Another external stakeholder is the regulator, with whom over the years, there has been growing desire to build a more collaborative and trust-based relationship. In addition, two important internal stakeholders are the business leaders, who want to understand how tax regulations will impact the business and the way business is conducted; and the employees whose profiles, as well as their expectations towards the organizations they work for, have changed over time.”

“What’s more, suppliers and the broader communities in which enterprises operate, are key to maintaining and building trust – which, in turn, gives the enterprise the opportunity to innovate boldly, grow responsibly, and create a new future”, adds Benny.

The characteristics of a trusted organization

“People trust organizations that demonstrate three key characteristics”, says Benny. “Such organizations display ability: they have the collective knowledge, skills, and abilities to reliably provide their products and services.

They show humanity, meaning that they not only care for the people involved in their transactions, but also for the overall community they do business in. Lastly, they demonstrate integrity and are respected for doing the right thing, take responsibility, and remain accountable.”

Data and technology bring new opportunities and risks

Benny: “Organizations are moving into a new digital era, which brings about new challenges. Digital transformation means connecting more people across the wider supply chain, so broader risks may arise when it comes to data breaches. To cope with these risks, organizations need to keep up with innovation in cybersecurity, which is its own area of expertise, requiring a specific mindset and skillset.”

Kathy: “In today’s landscape, it is difficult to talk about taxes without discussing data. Tax authorities are increasingly looking into more advanced tax data analytics. Corporations who have invested in technology to ensure robust tax data is available to support their tax positions, will earn the trust of regulators who will have greater confidence that a company is compliant or maintains tax positions that are reliable and accountable. In the future of tax data, we foresee regulators performing even more data analytics, automatically obtaining data on a real-time (or near real-time) basis, or even mandating the use of technological tools to be able to monitor, analyze, and control outcomes. ”

“In audit we are already using technology in this way”, continues Tim, “to undertake routine transaction work and enhance efficiency using robotics, as well as to analyze and correlate data to support opinions using data analytic techniques and Artificial Intelligence. Using technology this way helps to provide deeper insight on material value-related information provided to the market.”

How corporations build trust

“Trust is built upon consistently taking the right actions, like keeping data safe, delivering the right product at the right time, complying with regulations, and working with credible partners. One failure in a critical moment could undermine the reputation corporations worked hard for. As they say: trust is hard to gain, but easy to lose”, warns Benny. “That’s why it’s important to integrate security, compliance, and trust into all procedures, systems, and transformation activities.”

“From an audit perspective, building trust is our main goal”, says Tim. “An external audit is vital to the capital markets’ performance. Auditors build an objective and comprehensive view of all the risks and make their clients aware of possible risks and new challenges that could potentially result in losing the confidence of investors and other stakeholders. An audit should never be an end point – instead, it is the starting point of addressing weaknesses in internal inspections and governance mechanisms. Moreover, reporting has evolved to include more than historical financial information alone. Corporations have expanded their reporting responsibilities to cover non-financial information as well, detailing their commitments towards the market and future objectives. Think about sustainability reporting, where the need to improve the consistency, comparability and reliability of ESG reporting will be addressed with the new Corporate Sustainability Reporting Directive. The goal here is clear: helping stakeholders in their evaluation of companies’ non-financial performance based on reliable information and creating more transparency and comparability. When you do the right thing, trust between companies and stakeholders will follow.”

“Businesses need to consider certain key aspects when setting out their tax strategy”, adds Kathy. “The first step is defining a tax code of conduct – a mission statement and guiding principles on corporation’s tax management. Secondly, they should set out a tax policy framework, guiding how taxes will be managed throughout the organization. The third step is to set out a tax risk assessment framework, with procedures to identify, assess, and report tax risks across the compliance process. Finally, they will need to establish a tax control framework, setting out the controls and monitoring to operate the tax related processes, such as reducing the risk of non-compliance that may be the result of a lack of internal inspections or poor data quality. Introducing data techniques and data automation throughout the process helps organizations get ready for the future of tax.”

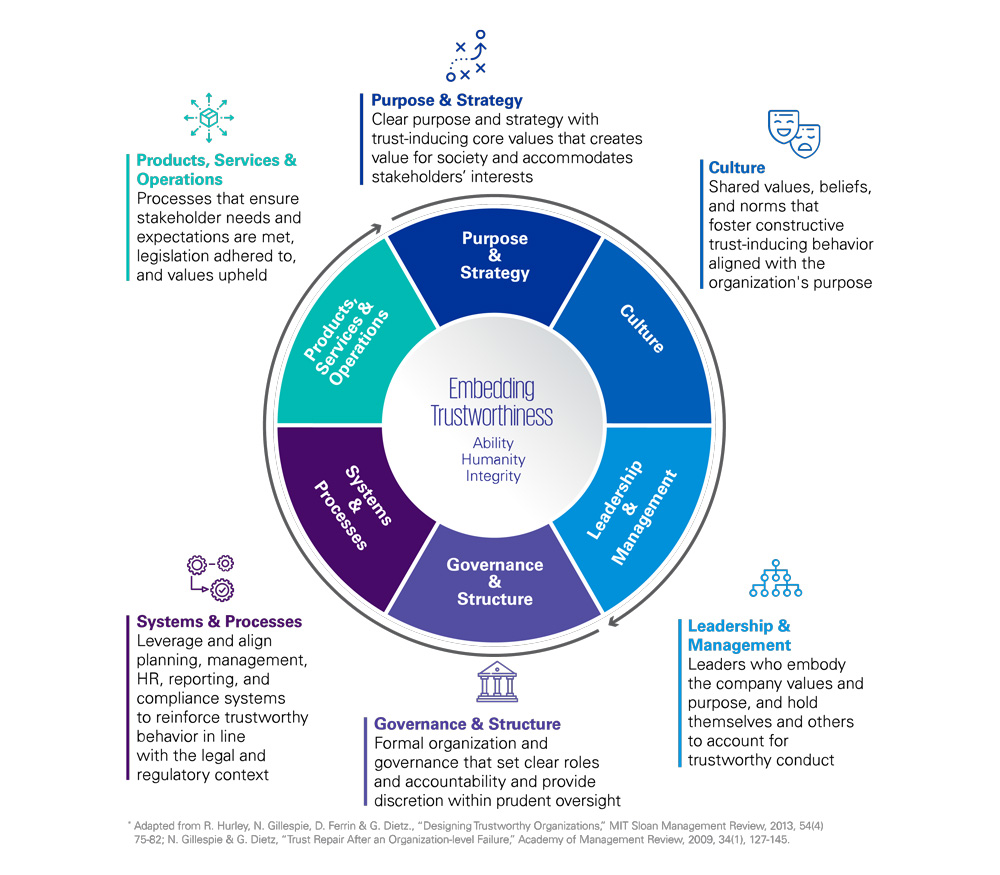

Multidisciplinary approach to cover all six elements of trust

When it comes to being considered as a trusted organization, there are six elements to consider. Together, they cover all domains – from strategy to leadership, from governance and structure to operations.

KPMG uses a multidisciplinary approach to maintain and build trust, and is a holistic provider with a global reach, bringing answers to challenges that organizations face – from digital transformation to audit and compliance, from advisory to tax and legal matters. We look beyond our singular expertise, connecting our partners and clients with the right knowledge within our organization and network.